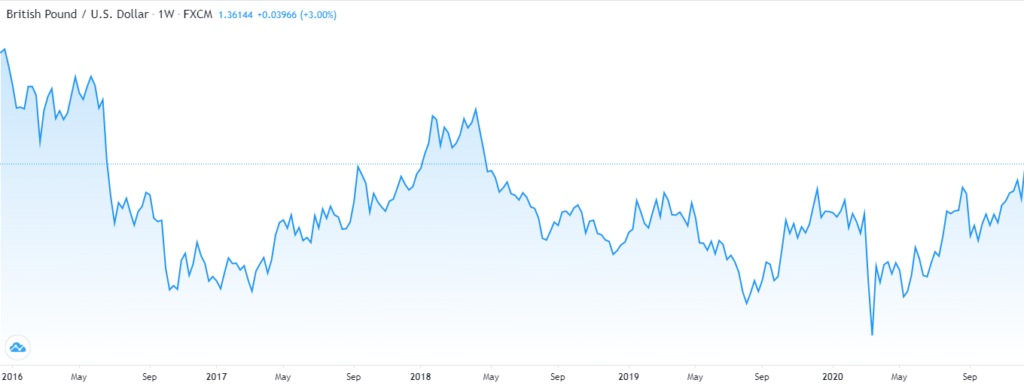

As many Indian traders will have noticed, Brexit has been the major driver behind the Pound Sterling’s (GBP) movements for the best part of four years now. The only greater influence has been the Covid-19 pandemic, and that was only briefly earlier this year.

Speculators in the GBP have been on a wild ride over the last few years. There was the Brexit referendum itself back in 2016 which sent the GBP off a cliff, followed by various attempts by Theresa May’s government to get a deal sorted – bringing a sense of optimism.

May’s winning but underwhelming display at the 2017 general election ensured that she could only ever govern with one hand tied behind her back. Her wafer-thin majority in the House of Commons meant that she needed the support of the most hard-line Brexiteers in her party. To placate them, she was forced into a much more aggressive stance in negotiations with the EU. Sterling speculators remained optimistic however – hopeful that her relatively conciliatory approach would eventually win out.

Out with the Old, In with the Boris

Eventually though, and in classic Tory fashion, the Conservative Party pulled the plug, and she was forced out. Her attempt to pass a withdrawal agreement was thwarted three times by her own colleaguesand she had no choice to resign. A victim of her own party’s failings – and Boris Johnson’s blind ambition to become Prime Minister.

GBP investors watched in horror as 2019 unfolded, with newly crowned PM Boris Johnson riding roughshod over parliamentary approvals and making it clear that any retreat from Brexit would be impossible. Following a convincing general election win last December, the GBP stabilised. After years of uncertainty, investors finally knew that Brexit was going to happen. Johnson promised it would be an orderly and managed exit from Europe, which was enough to calm an exhausted market.

The only thing business and investors hated more than Brexit was the uncertainty around Brexit. With the uncertainty removed the equation, the markets could start pricing costs in, and investors could make concrete decisions about the future. While it could not be called optimism, the markets were certainly relieved. But then the rumours started of a new virus in China.

COVID-19 + Brexit = Volatility

It is safe to say that GBP traders did not expect to 2020 to be quite this volatile. The March lockdown in the UK sent the GBP plunging as investors rapidly tried to price in the effects of one of the largest economies in the world coming to a screeching halt. The summer months brought a recovery, and the Brexit news helped. It looked like the EU and Boris Johnson’s government were going to come to an ill-tempered compromise. This was lessened by the UK government’s threat to break international law by unilaterally ignoring sections of the Withdrawal Agreement it signed with the EU. But overall, things were looking up.

Summer turned to autumn, and autumn turned to winter. Infection rates started rising again, Boris Johnson’s government provoked controversy after controversy, and still the EU and the UK could not reach any agreement on fishing rights in the North Sea.

As we come into the last few days of the year Brexit negotiations have been beset by reports of gunboats being deployed in the North Sea and long delays at British ports. Both sides have made it clear that there are still significant differences between the two sides. The European Parliament has intimated that it will not ratify any deal before the New Year. But still the GBP climbs against the USD.

‘The Boy Who Cried Wolf’ Effect

Markets have refused to take any of these negative reports at face value. Investors and speculators have given up trying to make sense of any public statements from either side in the negotiations. In the absence of any believable information from the two parties, prevailing wisdom seems to be that the price of a no-deal is too big to pay for either side.

Forex traders in the UK are leading a surge in long positions on the GBP, suggesting that a deal is fully priced in. The danger of course is that we could be looking at a classic case of the ‘Boy Who Cried Wolf’ effect. In the original tale the boy lied about the wolf’s existence so many times that the one time he was being honest the entire village refused to listen to him. So, when von der Leyen and Johnson warn of real possibility of a no-deal – or an ‘Australian-style deal’ as Johnson calls it – is the wolf finally and truly at the door? The markets do not seem to believe it. But if they are wrong the GBP is in for a colossal collapse once the markets re-open on January 2nd, 2021.

")