The 21st century has undoubtedly seen all the catchy headlines about blockchain technology, thanks to the rise of cryptocurrency, namely Bitcoin. But as popular of a topic Blockchain technology is, it wouldn’t be an overstatement to say that the knowledge and understanding surrounding it is still rather limited.

In this article, we are going to be covering some key concepts such as:

- what is blockchain technology

- cryptocurrency and Bitcoin

- when it was introduced and by whom

- how it works and why it’s different

The Basics of Blockchain

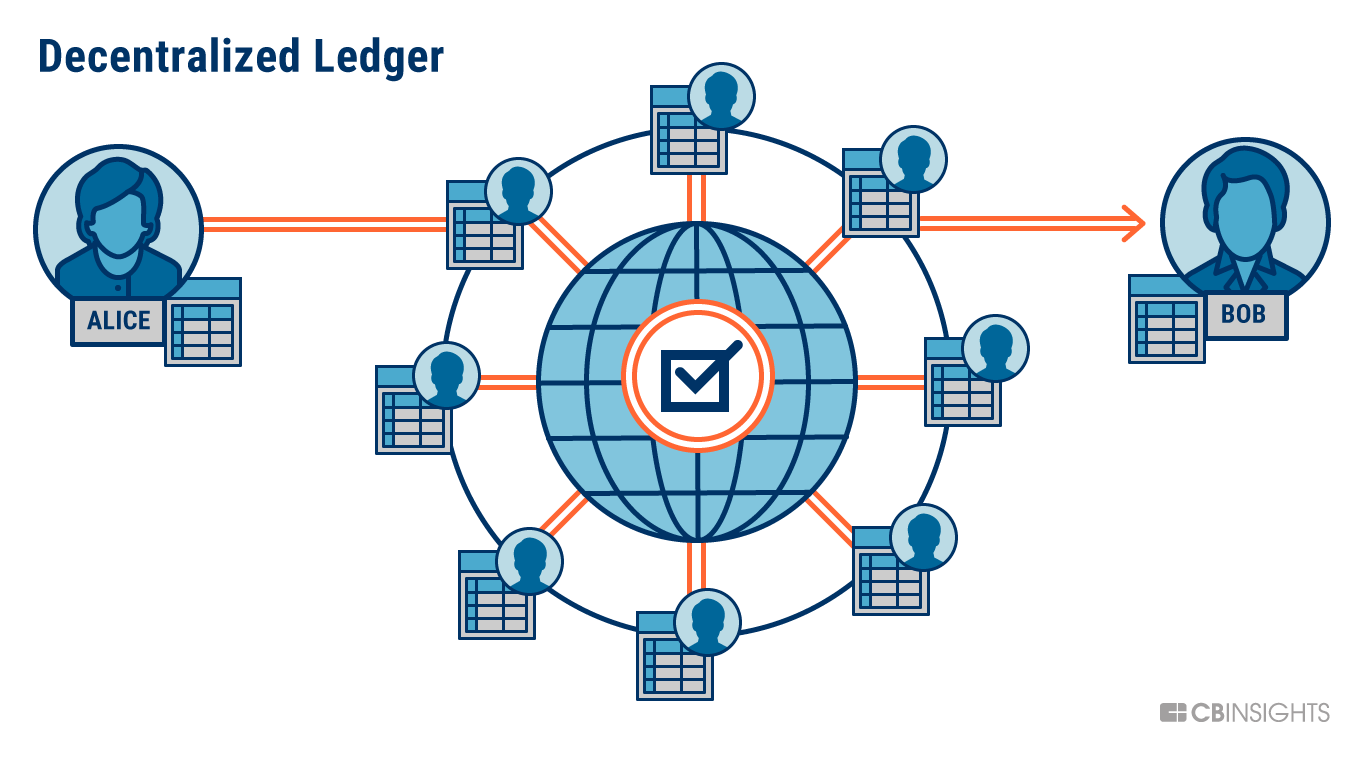

Let’s start with a definition. The blockchain is an unalterable ledger record of bundles of transactional data managed by a cluster of computer systems and is not owned or regulated by any single entity or government body.

Now, let’s break it down.

As per Maodong Xu, Blockchain is exactly what its name suggests: block-chain, as in a ‘chain’ of ‘blocks’. Now, a ‘block’ is nothing but a number of transactions bundled together. This bundle or ‘block’ is then linked to other bundles which results in a chain-like structure. A good example would be beads on a necklace.

Whenever a new block is linked to other blocks, it becomes a part of the blockchain and becomes resistant to modifications. Alteration in a block can’t be made without altering all subsequent blocks. Because of this quality, blockchain technology is said to be highly-secure, highly-accountable, and very reliable since the transactions made are locked in code.

The History of Blockchain and Cryptocurrency

The most common misunderstanding when talking about the terms ‘blockchain’ and ‘cryptocurrency’ is that people think they are identical and can be used interchangeably. That’s not true. Blockchain is a technology.

Cryptocurrency is an application built on top of the Blockchain technology.

Blockchain technology is not something that is limited to just cryptocurrency, albeit, it was indeed built for that purpose in 2008, although the idea of it was outlined as early as 1991 by two researchers named Stuart Haber and W. Scott Stornetta.

Well, then that raises the question: who created cryptocurrency?

The first cryptocurrency, Bitcoin, is said to be the creation of Satoshi Nakamoto – a presumed pseudonym used to mask the identity of the person or group of people who invented Bitcoin in order to remain anonymous.

The true identity of Satoshi Nakamoto remains unknown to the world till date. At the time of the 2008 financial crisis – a time which affected the world’s economic systems pretty badly – people were quite upset at banks and governments, unsurprisingly so.

With the crisis came along the increasing distrust of citizens towards these financial bodies – that which were completely outside their control whatsoever. As a natural consequence, people began to grow resistant towards these institutions and Bitcoin was born.

Eventually, more people started buying into its idea of cryptocurrency since it offered them what banks couldn’t: complete control over their own money. Soon after the invention, Bitcoin was termed as “the future of money,” leading to its rapid popularity and the advent of many other blockchain startups, Islamic Blockchain is just one such cryptocurrency.

Since Bitcoin is a peer-to-peer currency, it allowed people to engage in financial transactions without depending on banks, governments, or any other middle party. Also, any transaction made was incredibly secure and verified due to cryptography.

Via Bitcoin, people could transact with anyone, anywhere, anytime, and without having prying eyes invade their privacy and security. This idea of potential termination of systemic unfairness caught on to people and the value of Bitcoin skyrocketed within a few years.

How blockchain works and why it is different

Blockchain technology is different from traditional banking system mainly because of the following qualities:

- Decentralization

- Transparency

- Anonymity

- Immutability

Let’s take a look at each of these qualities in detail and compare them with the traditional banking system.

Decentralization

In order to understand how blockchain works, it is better if we see it in the context of how it is used by Bitcoin and compare it with fiat money. As an example, whenever you make a transaction via cash, say at a grocery store, the money passes through 3 parties: you (sender), your government (intermediary), and the store (recipient).

Here, the actual control of the currency note is in the hands of the government who decides the validity and value of your money. Plus, you cannot use that currency anywhere outside of your own country.

Therefore, it is a centralised system. With Bitcoin, however, there is no middle party involved which allows for direct transactions between two entities. The transactions are simply made possible via a global network of computes called “nodes.”

Also, unlike fiat money, Bitcoin has no physical form and is international. It is not limited to any specific country or region. Therefore, it is decentralised system allowing for a distribution of control i.e. people having power over their own money.

Transparency

Perhaps the most beneficial quality of blockchain technology in terms of accountability is that they the transactions made and recorded via them are transparent and trackable.

Any transaction made via Bitcoin’s blockchain can be viewed via blockchain explorers or by having a personal node. This means that you can basically track every Bitcoin in the world. Cool, right?

Anonymity

Transaction within the blockchain are made possible with the help of keys: public and private key. For simplicity of understanding, think of a public key like your bank account number and your private key like your password.

You send your public key to whoever you wish to transact with. The private key stays only with you – shared with no one and kept safe and hidden. You don’t need to register yourself anywhere or use your personal IDs, allowing for anonymity.

This feature of blockchain is a little controversial, though.

As convenient as it is to not have to use your identity, it’s true that this feature has given leverage to crimes like money laundering and even terrorism. Fortunately, organisations like the FATF (Financial Action Task Force) work with countries all around the world to help develop policies to protect the global financial system against these crimes.

Immutability

Transactions made within the blockchain network are stored in blocks and locked in mathematical code. They are virtually impossible to be tampered with. Alteration in any one block would require an alteration in all the subsequent blocks. This immutable quality of blockchain transactions make them incredibly secure and highly reliable.

Conclusion

Blockchain is certainly an area of interest for many of us and it’s catching new eyes every day. For when it was created to how it works, the idea is undeniably new and exciting especially for the tech-heads among us.

We hope this article was able to help you learn the basics of blockchain, its role in cryptocurrency, its qualities, and give you a vision of where it might lead the world. Thank you for reading!

")